Policy Memo

Topline

The Social Security Trustees 2026 Report shows that Social Security is running out of time and money. Insolvency is coming.

The Social Security Trustees 2026 Report shows that Social Security is running out of time and money. Insolvency and automatic 22 percent benefit cuts are projected for 2032, meaning everyone from Gen X and younger is on track to not receive a single full Social Security benefit. Without reform, America’s favorite entitlement program will become its most disgraced.

Social Security is a nearly universal entitlement program and reform is inevitable, so it is helpful for Americans to understand some basic aspects of the program and the options for reform. Here are nine things every Americans should know about Social Security and the Trustees 2026 annual report:

Since Social Security’s inception in 1935, the program’s financing has been kept separate from other government spending. For decades, Social Security’s trust fund accumulated large surpluses meant to fund future benefits. As benefits grew faster than tax revenues, Social Security’s costs began exceeding its tax revenues in 2010, and the program has been drawing down on its trust fund reserves to maintain full benefits since then. In the fourth quarter of 2032, the trust fund will run out of money and effectively cease to exist as all revenues will go towards expenses. At that point, everyone of Generation X and younger will not have received a single full benefit.

Because Social Security’s finances are separate and the program cannot pay out more in benefits that it has in reserves and from tax revenues, current law requires a 22 percent reduction in Social Security benefits beginning in the fourth quarter of 2032. (Note that the Congressional Budget Office projects a significantly larger 28 percent cut will be necessary in 2032). Unless Congress specifies, those cuts will presumably be across-the-board, applying equally to everyone from ages 62 to 102, and regardless of whether someone has $200,000 or $20,000 of annual income. For an average beneficiary who receives $2,000 per month, a 22 percent reduction will amount to about $5,300 less per year. Over time, necessary benefit cuts will rise from 22 percent to 38 percent in 2100.

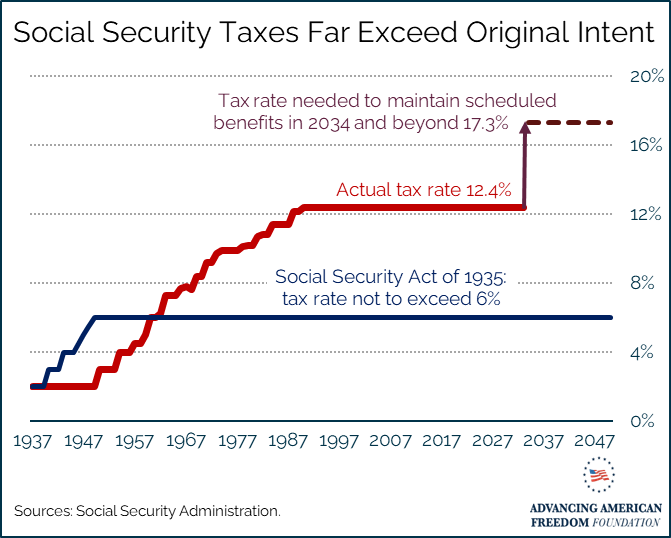

Social Security was a Great Depression-era program intended to protect older Americans from outliving their savings and to protect younger generations from having to pay for welfare for impoverished elderly people. Social Security started out as a 2% tax and the program promised to never take more than 6% of workers’ paychecks. Today it takes 12.4% and in 2034, it would require 17.3% of workers’ paychecks to maintain current benefits. The combination of benefit increases, program expansion, and increasing life expectancies have caused Social Security’s costs to explode.

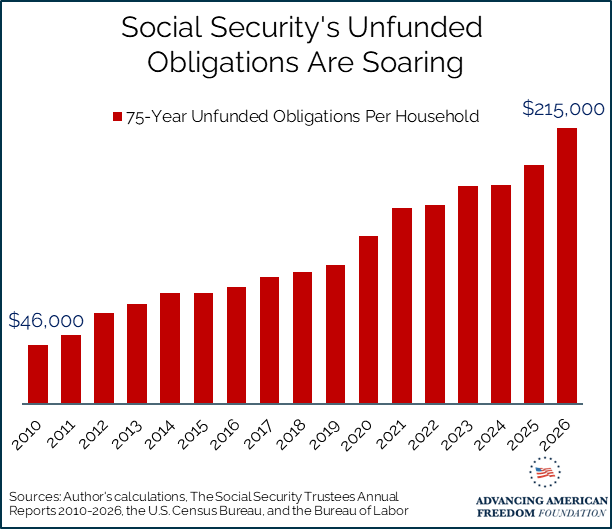

The present value of Social Security’s 75-year unfunded obligations—essentially the difference between scheduled and payable benefits over the next 75 years—equals $29.3 trillion or $215,000 per household. That is up by $4.2 trillion, or an extra $29,000 per household since just last year.

Preventing any benefit reductions would require immediately raising Social Security’s tax rate from 12.4% to 16.65% (a 34 percent increase). This would cost a median household with $84,000 of income about $3,600 more per year, and $14,000 total in annual Social Security taxes. If those taxes were set aside in a personal retirement account, they would generate enough money to replace upwards of 130% of the household’s income in retirement. That compares to Social Security’s average 40% income replacement rate.

The trustees noted positive impacts on the program’s finances due to improved economic assumptions, and negative impacts from recent legislation and changes in demographic assumptions. That includes an increase in assumed productivity growth and real average earnings growth. While not specifically noted, those changed assumptions likely stemmed from the positive economic impacts of lower taxes enacted in the One Big Beautiful Bill (OBBB).

The OBBB tax cuts also had a negative impact on the trust fund by reducing taxes on Social Security benefits. Moreover, the Social Security Fairness Act that Congress passed at the end of 2024—which provides windfall benefits to certain public sector workers who were exempt from Social Security taxes—increased Social Security’s costs by about $200 billion and took six months off the trust fund’s solvency.

Changes to demographic assumptions reduced Social Security’s fiscal outlook. That included a reduction in the long-run total fertility rate, from 1.9 in last year’s report to 1.75 in this year’s report (the actual fertility rate for 2025 is estimated at 1.59). It also included a significant reduction in the estimated number of temporary or unlawfully present immigrants in 2035 and later, from 1.35 million to 1.2 million.

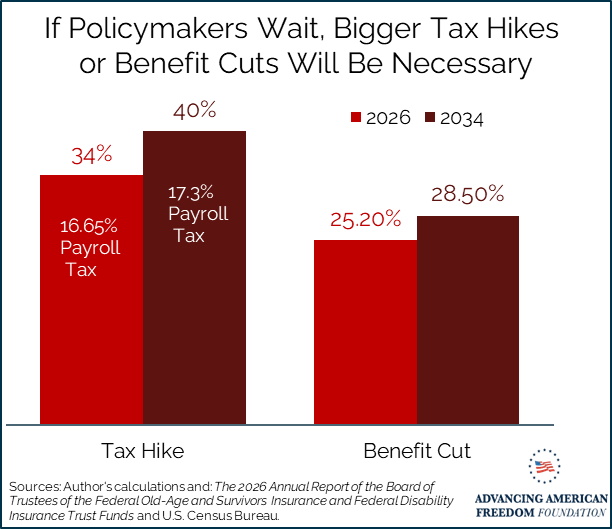

If policymakers wait until 2034 to make changes—a date that would be possible if Congress passes legislation to let Social Security’s old age and survivor’s insurance program use up the disability insurance program’s trust fund—maintaining long-run solvency would require larger tax hikes or benefit cuts. Whereas a 34 percent tax increase, from 12.4% to 16.65%, enacted in 2026 would maintain long-term solvency, a 40 percent tax increase, from 12.4% to 17.3%, would be necessary in 2034. Alternatively, while a 25.2 percent benefit cut enacted in 2026 would maintain long-term solvency, a 28.5 percent cut would be necessary in 2034.

Social Security’s financial challenges are occurring against the backdrop of an unsustainable $39 trillion-and-growing federal debt and a declining fertility rate that means fewer worker have to support more retirees. With Social Security and interest payments on the debt costing $2.7 trillion, or nearly $20,000 per household in 2026, unsustainable spending and debt are already putting a strain on younger Americans who are trying to get married, buy homes, and start families.

Social Security’s insolvency in 2032 could coincide with the federal government running out of fiscal space, entering a debt spiral, and losing the ability to borrow at reasonable interest rates. If that happens, it will be too late for policymakers to enact measured Social Security reforms that minimize benefit cuts. It would also make it extremely costly and risky to attempt short-term fixes like a deficit-financed general fund transfer, which could further reduce market confidence in the U.S.’s ability to meet its debt obligations.

On the other hand, enacting Social Security reform in the near future would ease the growing threat of a fiscal crisis by reducing projected spending growth and signaling a commitment to long-term budget sustainability. This would help preserve fiscal flexibility, giving policymakers greater capacity to respond to future economic downturns, national emergencies, and geopolitical challenges

By gradually shifting Social Security back to its original intend of poverty prevention in old age, policymakers can better target benefits toward those who need them most, while reducing Social Security’s burden on current and future workers. This would strengthen economic growth by increasing saving, investment, and labor-force participation. According to an analysis by the Penn-Wharton budget model, a smaller and better-targeted Social Security program could increase long-term GDP by 5.3 percent, while a larger program would reduce GDP by 1.0 percent. This would translate into a gain of about $4,000 per year in median household income across the United States.

Social Security’s $29.3 trillion shortfall ($215,000 per household) won’t fix itself. Lawmakers can either allow automatic 22 percent benefit cuts in 2032 or enact gradual, targeted reforms now to protect lower- and middle-income retirees, strengthen the economy, and demonstrate fiscal fortitude before markets force abrupt action.