Congress should seek to go big on reconciliation 2.0: funding the Department of Homeland Security (DHS), implementing portions of the Safeguard American Voter Eligibility (SAVE) Act, defunding abortion providers, passing pro- growth tax reforms, reducing wasteful and fraudulent spending, and encouraging deregulation. This report highlights 20 policy items that legislators should work to include in reconciliation, as well as a procedural consideration to ensure that abortion providers remain defunded and their federal funding prohibition does not expire.

BACKGROUND

Elected Senate Democrats have refused to pass new appropriations to fully fund DHS. In response, there are now calls to provide the needed DHS funding – in particular, for Customs and Border Protection (CBP) and for Immigration and Customs Enforcement (ICE) – through a reconciliation bill, which can bypass the Senate filibuster and allow passage with a simple majority. Congress, however, has limits on how often it can consider and pass a reconciliation bill.

While some are calling for a narrow reconciliation bill that only covers DHS funding, reconciliation provides a rare opportunity to enact other policies as well. There are calls to add parts of the SAVE Act and needed defense investments to the bill. Beyond that, a new reconciliation bill could build on the legacy of the One Big Beautiful Bill (OBBB, also known as the Working Families Tax Cuts) by enacting more pro-growth tax reforms, reducing wasteful and fraudulent spending, encouraging more deregulation, and further facilitating enforcement of immigration law.

This report outlines 20 policy items that lawmakers should consider including in a new reconciliation bill and discusses potential options that Congress has in how it can craft budget resolutions to unlock the reconciliation process for one or multiple bills.

MENU OF SPENDING OPTIONS FOR RECONCILIATION 2.0

Extend the Existing Ban on Federal Funding for Abortion Providers

Background: The One Big Beautiful Bill (OBBB) included a one-year ban on Medicaid funding from going to entities that provide abortions that expires on July 4, 2026.

Congress should:

- Permanently ban federal abortion funding or, at a minimum, extend OBBB’s temporary ban.

- (Alternatively) If Congress were limited to a revenue-only reconciliation bill, an alternative method would be to impose a new tax on abortion providers that is equal to the total of any funds they receive from Medicaid in a given tax year (which could be collected either annually or quarterly). This would have the same impact as the spending provision that was included in OBBB but do it in a manner that is compliant with reconciliation instructions that allow only revenue provisions.

Strengthen Voter Integrity through Address and Citizenship Verification

Background: The National Voter Registration Act, 52 U.S.C. § 20507(c), authorizes the use of the National Change of Address database of the U.S. Postal Service (USPS) by states to verify changes of residential addresses by registered voters. The USPS has special procedures for the expedited handling of all election-related mail.

Congress should:

- Provide funding for the USPS to automatically notify state and local election officials when election-related mail provided to USPS by such officials for delivery is being sent to an individual who the NCOA database shows has changed his or her address, including providing the new address and the date it was changed.

- Provide funding for the Department of Homeland Security and the USPS to share data between the NCOA database and DHS’s Systematic Alien Verification for Entitlements database to provide NCOA with citizenship status information on all individuals within the NCOA database, and to provide funding for the USPS to automatically notify state and local election officials when election-related mail provided to USPS by such officials is being sent to an individual that the supplemented NCOA database shows is not a U.S. citizen.

Tie Medicaid FMAPs to States’ Improper Payment Rates

Background: In recent years, Medicaid has reported improper payment rates between five and nine percent (between $31 billion and $50 billion per year), but those are based on only partial measurements. Years with more complete measures revealed improper payment rates in excess of 25 percent, or roughly $100 billion per year. States face no consequences when they issue improper payments; instead, the incentive is to spend more, check less, and pass the buck to federal taxpayers.

Congress should:

- Hold states accountable for their errors and negligence.

- Ensure that for each percentage point that a state’s improper payment rate exceeds a 3 percent cap, the state’s Federal Medical Assistance Percentage (FMAP)—which is the portion of Medicaid spending paid by the federal government—be reduced by one percentage point (for both traditional and expansion enrollees).

- Ensure that a true improper payment rate is obtained by requiring better Payment Error Rate Measurements (PERM) including: measuring every two years instead of three, counting payments from Medicaid Managed Care Organizations (MCOs), and measuring eligibility errors based on federal eligibility standards.

- Subtract one percentage point from a state’s FMAP if it does not obtain annual, opt-in consent from Medicaid Home and Community Based Service providers before taking union dues out of their Medicaid payments.

This could save between $20 billion and $60 billion per year.

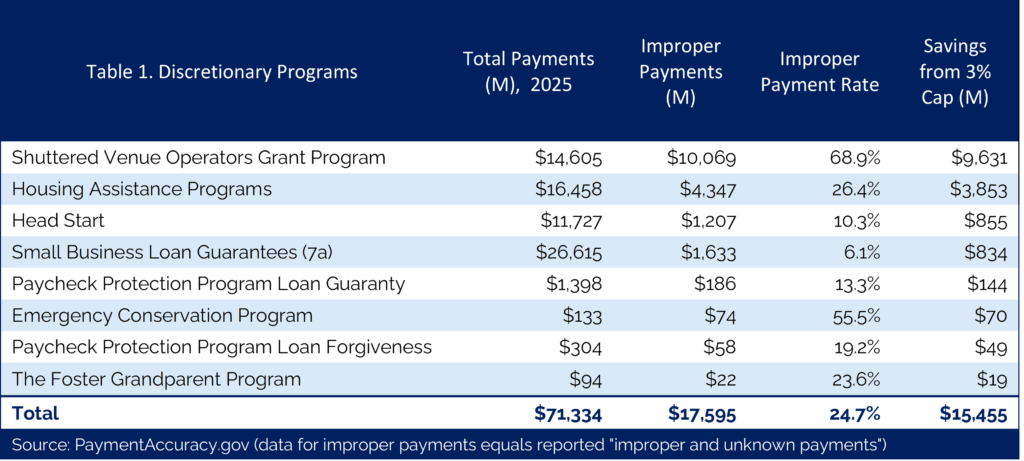

Charge States for Excessive Improper Payment Rates

Background: The federal government reported $184 billion in improper payments in 2025. This includes over $71 billion from just a handful of discretionary spending programs.

Congress should:

- Measure the total amount of improper payments in each state’s federally funded and state-administered discretionary programs and reduce federal Medicaid funds for expansion enrollees by $1 for every $1 by which the state’s total improper payments exceed a 3 percent cap.

- This should include measuring improper payments in currently unmeasured programs such as LIHEAP, CDBG, and the BEAD Program.

This could save upwards of $15 billion per year.

Eliminate Broad-Based Categorical Eligibility in Federal Welfare Programs

Background: Broad-Based Categorical Eligibility (BBCE) allows states to deem households eligible for food stamps based on the receipt of a nominal TANF benefit (such as a brochure or access to a 1-800 number) while skipping over federal income and asset limit requirements. This has allowed an additional 5.6 million otherwise ineligible individuals to receive food stamps, and it has caused significantly higher improper payment rates.

Congress should:

- Require states to follow federal eligibility standards for food stamps. The No Welfare for the Wealthy Act of 2025 (H.R. 416) does this.

This could save about $10 billion per year.

Require States to Report Beneficiary Information for Federally-Funded Programs

Background: A lack of data on who receives federally-funded and state-administered benefits restricts the government’s ability to identify and eliminate improper payments.

Congress should:

- Condition states’ eligibility for federally funded welfare benefits on states’ reporting of basic beneficiary information to the federal government, where it can be collected in a central database that will allow state and federal governments to better identify and limit improper payments.

Expedite Accountability and Work Requirement Provisions from H.R. 1

Background: H.R. 1 included significant reforms to limit the federal government’s share of states’ improper payments in food stamps and those based on Medicaid eligibility errors, but these provisions do not kick in until 2028 for food stamps and 2030 for Medicaid.

Congress should:

- Expedite the implementation of state cost-sharing for their improper food stamp payments to 2027 and move the Medicaid eligibility limits up to 2028.

Fund Programs to Eliminate Waste, Fraud, and Abuse

Background: Congress has a long history of funding programs that have successfully improved the operations of federal grant and welfare programs and that have eliminated more waste, fraud, and abuse than the cost of funding these program-integrity activities. As such, providing funding for these operations not only removes wasteful spending and reduces fraud, but can also serve as a pay-for inside of a reconciliation bill.

Congress should:

- Provide funding to eliminate waste, fraud, and abuse along the lines of the programs and practices laid out in this GAO report: Health Care Fraud and Abuse Control Program Report (Fiscal Year 2023)

MENU OF REVENUE OPTIONS FOR RECONCILIATION 2.0

Link Trump Account Donations to Expanded Death Tax Exemptions

Background: OBBB created Trump Accounts, tax-advantaged savings accounts for kids under 18. While there is a modest tax advantage for investments once in the accounts, there is no tax incentive for people who give to the accounts. The current Death Tax exemption is $15 million. The interaction of the Death Tax and the way charitable giving is handled in the tax code incentivize wealthy Americans to donate to and through foundations or donor-advised funds instead of, for example, giving direct donations to the Trump Accounts of tens of millions of American children.

Congress should:

- Allow individuals (not just foundations) to make equal donations to children’s Trump Accounts in ZIP codes and age ranges of their choice.

- Increase individuals’ allowable Death Tax exemptions by 55.5 percent of such donations to groups of (non-familial) Trump Accounts.

- With a Death Tax rate that quickly ramps up to 40 percent on net assets above the exemption amount, the higher exemption provided here would offset the combination of income and death taxes otherwise assessed such that the tax break for donating to non-familial Trump Accounts would now roughly be on par with the value of tax breaks that are currently offered for other forms of giving.

Extend Expensing for Factories

Background: Congress passed full expensing for factories in OBBB to let companies immediately deduct the full cost of building structures used in the manufacturing, production, or refining of tangible property when those structures are placed in service (instead of spreading deductions over a 39-year period—2.5 percent per year). This provision, to allow for full and immediate expensing, removes a layer of double taxation that specifically penalizes building factories, refineries, and other industrial and agricultural buildings in America. However, this expensing provision for factories in OBBB is set to expire for structures on which construction begins after December 31, 2028, or that are placed in service after December 31, 2030. Planning and execution of major construction projects often lasts many years (let alone dealing with federal and state-level permitting and other regulations), so the early sunset diminishes the provision’s value.

Congress should:

- Permanently extend factory expensing or at least extend out its sunset date.

Make the Section 179 Deduction an All-Purposes Expensing Account

Background: The Section 179 deduction is an expensing provision that is geared toward small and midsize businesses. It can be used for certain building improvements (e.g., roofs, HVACs, security and fire alarm systems), as well as certain off-the-shelf software that otherwise would have to be depreciated. OBBB raised the maximum annual Section 179 deduction to $2.5 million (with a phaseout beginning at $3.13 million, as of 2025).

Congress should:

- Broaden the Section 179 deduction to make it an all-purpose expensing account for any costs that would otherwise be depreciated over multiple years (up to the $2.5 million limitation). This would include providing full and immediate expensing for all construction done by these small businesses (up to the deduction limit).

- (Alternatively) Lock in permanent, full expensing for small and midsize businesses under the Section 179 deduction.

- Remove the phaseout or at least consider a more gradual phaseout for the Section 179 deduction. The phaseout is related to the size of certain investments made by these companies in expanding productive capacity. It therefore penalizes good investments and would need to be amended if Congress expanded what Section 179 could be used to cover.

Impose Payroll Tax on Firms that Employ Illegal Immigrants

Background: Legally, companies cannot knowingly employ non-citizens who lack authorization to work in the United States. Employers can face penalties if they violate rules for verifying the status of their workers. However, such penalties are relatively modest and only sporadically enforced.

Income is subject to federal income and payroll taxes regardless of its legality, including illegal immigrants working in the U.S. without authorization. To encourage tax compliance, the IRS is bound by strict rules against sharing tax information with immigration enforcement agencies and others outside of specific authorized purposes.

Congress should:

- Impose a 15% payroll tax on firms that pay non-citizen employees who lack authorization to work in the United States and employees whose authorization to work in the U.S. has not been confirmed via E-Verify.

- If at any point, it is discovered that a firm didn’t comply with this payroll tax on wages paid to employees with unverified status, the employer should be liable for the tax retroactively, with interest and a penalty equal to 500% of the unpaid tax.

Allow Full Expensing for Contract R&D Conducted in Strategically Allied Nations

Background: OBBB enacted full and immediate expensing for R&D that is conducted in the United States. However, multinational companies that conduct R&D outside the U.S. still must use 15-year straight-line amortization. When U.S.-parented multinationals conduct R&D outside the U.S., this is often in a contract R&D arrangement where the resulting intellectual property (IP) accrues to the U.S. parent. This includes many of the most cutting-edge industries and many of our defense industrial producers who, in coordination with the federal government, co-research and co-produce military equipment with such partner nations.

Congress should:

- Allow full and immediate expensing for contract R&D performed outside the U.S. if it is conducted in a permissible country and the resulting IP will be owned by the U.S. company.

- Define permissible country to exclude Foreign Entities of Concern (15 U.S.C. §4651) and to include only countries that have a free trade agreement and/or tax treaty with the United States or countries covered under the parameters laid out in 10 U.S.C. § 2350a – (Cooperative research and development agreements: NATO organizations; allied and friendly foreign countries).

Impose Payroll Tax on Firms that Employ Workers with No or Unverified Work Authorization

Background: Legally, companies cannot knowingly employ non-citizens who lack authorization to work in the United States. Employers can face federal penalties if they violate rules for verifying the authorization status of their workers. However, in most cases such penalties are relatively modest and only sporadically enforced.

Income is subject to federal income and payroll taxes regardless of its legality, including illegal immigrants working in the U.S. without authorization. The IRS is bound by strict rules against sharing tax information with immigration enforcement agencies and others outside of specific authorized purposes. The IRS already collects taxes from both workers that are not legally authorized to work in the U.S. and their employers. However, there is no extra tax-related penalty on these unlawful arrangements.

Congress could remedy this and 1) raise more revenue, 2) provide extra penalties for breaking immigration law, 3) remove some of the monetary imbalances that favor hiring illegal workers over citizens and those that are authorized to work in the U.S., and 4) encourage more employer compliance with U.S. immigration law.

Congress should:

- Impose a new tax on the wages paid to non-citizen employees who lack authorization to work in the United States and employees whose authorization to work in the U.S. have not been confirmed via E-Verify. This tax could be withheld from paychecks by the employers and be in the range of perhaps 15 percent to 21 percent (21 percent would match the corporate income tax rate since many of these firms already unlawfully deduct these wages and avoid paying corporate income taxes on an equivalent amount of money).

- If at any point it is discovered that a firm did not comply with this new payroll tax, the employer should be liable for the unpaid tax retroactively, with interest and a penalty equal to 500 percent of the unpaid tax.

- Provable use of E-Verify for all potential hires could be offered as a legal safe harbor from facing the penalties under this new tax.

Count Green Tax Credits as Taxable Income or Repeal Them Entirely

Background: The Inflation Reduction Act of 2022 ushered in more than $1 trillion of subsidies for green energy over 10 years, mostly in the form of tax credits. OBBB terminated, restricted, and accelerated the phaseouts of many of these credits (about $500 billion over 10 years). However, some green tax credits survived, and it grandfathered in some companies already taking advantage of the credits.

Congress should:

- Count all remaining green tax credits received by businesses as taxable income.

- This would effectively offset 21 percent of the value of corporate tax credits in many cases (more when credits are taken in lieu of deductions).

Or, alternatively:

- Terminate all federal energy subsidies, including for:

- The manufacturing of wind and solar components (45X Credits),

- Grandfathered subsidies for the production of and investments in wind, solar, and other “green” energy sources (45Y and 48E Credits),

- Subsidies for zero-emission nuclear power production (45U Credits),

- Subsidies for the production of green hydrogen (45V Credits),

- Clean fuel production (45Z Credits), and

- Carbon oxide sequestration (45Q Credits).

Allow Shipbuilders to Pay Distributed Profit Tax (Ideal Policy) Instead of Income Tax

Background: When companies retain earnings, those earnings are subject to income tax, whereas amounts they spend on company operations, for example, can be deducted. Taxes on retained earnings are not especially problematic for businesses that do not require large periodic capital investments. However, taxing retained earnings is much more problematic for shipbuilders, who may need to set aside hundreds of millions or billions of dollars to build a single ship.

Congress should:

- Give corporate shipbuilders the option of paying a flat 21 percent tax on distributed profits instead of paying the corporate income tax.

- Under a distributed profits tax, retained earnings are not taxed, but rather the tax is triggered when companies distribute profits to shareholders through, for example, dividends or stock buybacks.

- A distributed profits tax is sound tax policy that could replace the entire business tax code (though less easily). Setting up a distributed profits tax for shipbuilders could act as a pilot program for a broader reform.

- This would be an economically sound way to encourage American shipyards to expand operations and to enhance this critical industry.

Index Capital Gains for Inflation

Background: Property that is sold for more than its value when it was acquired is generally subject to capital gains taxes. The increase in an asset’s price may reflect real appreciation in its value, but it may also reflect inflation. Capital gains taxation in the U.S. does not differentiate between real gains and inflation. Taxing inflation can lead to significantly higher taxes on capital gains that produces a lock-in effect where investors and other individuals tend to simply hold onto assets—either to avoid paying taxes in the short-term or to escape taxes entirely by passing the gains on as inheritances—rather than selling them when it would otherwise be economically advantageous to do so. This lock-in of investments and financial assets reduces economic dynamism.

The tax code allows an exemption of $250,000 (or $500,000 for married joint filers) for the sale of homes that are the primary residence of the seller before capital gains taxes start to apply. To qualify for the full exemption, the taxpayer must have lived in the residence for at least two of the last five years. Capital gains taxes (including inflation) discourage seniors and empty nesters who have lived in their homes for a long time from downsizing, even when it would otherwise be right for their situation, effectively leading to lower housing supply among other issues.

Congress should:

- Allow all capital gains to be indexed for inflation from the time that an asset was acquired.

- (Alternatively) Allow capital gains on primary residences to be indexed for inflation to encourage more housing turnover and to better match supply and demand.

- (Alternatively) Allow capital gains on all real property to be indexed for inflation to encourage more construction and also to unlock commercial properties and incentivize more re-shoring of manufacturing in addition to increasing housing turnover.

Condition Municipal Bond Exclusion on School Choice

Background: Interest earned on state and local municipal bonds is currently untaxable under the federal income tax. This contrasts with most interest income, which is taxable. This discrepancy in tax treatment makes municipal bonds relatively more attractive, especially to individuals, businesses, and institutional investors in high tax brackets. As a result of this tax preference, state and local governments can issue debt at a lower interest rate, while corporate bonds, for example, must overcome this tax difference by paying out higher interest rates. In this way, the tax advantage for municipal bond interest incentivizes state and local governments to take out more debt, while simultaneously crowding out private borrowing and investment.

A large share of municipal bonds goes to funding public schools.

Congress should:

- Make interest income received on future issues of municipal bonds taxable, unless:

- The state from which the bond was issued has enacted one or more specified school choice programs that are available to at least 40 percent of the state’s school age children based on the determination of the Secretary of Education, and

- The average amount spent by the state on school choice students is at least 60 percent of the amount the state spends on average for the education of non-school choice students.

- The specific parameters could vary. A version of this proposal is included in Section 5 of the Achieving Choice in Education Act.

Raise the $5,250 Annual Exclusion for Employee Upskilling to $15,000

Background: The Revenue Act of 1978 allowed individuals to exclude from their taxable income certain qualifying employer-provided educational assistance. This could include tuition, fees, and supplies and equipment. Recent changes have also allowed employers to offer student loan assistance under this provision. However, the maximum exclusion amount remained unchanged at $5,250 from 1987 through 2026, even as educational costs have skyrocketed. OBBB finally added an inflation adjustment beginning in 2027 but did not adjust retroactively for inflation over the past 40 years.

Congress should:

- Raise the maximum employer educational assistance exclusion to $15,000 to roughly account for the inflation since it was last adjusted.

Tax Credits to Offset Regulatory Penalties

Background: Deregulation often requires going through the same complex rulemaking process that is required to make new regulations. This has made it much easier for the unelected federal bureaucracy to add to the regulatory code over time and made it much harder for sweeping deregulation to occur. However, many federal regulations are enforced only through the imposition of monetary penalties, which Congress could remedy through reconciliation.

Congress should:

- Zero out penalties for certain regulations or provide a tax credit to businesses to offset the penalty of those regulations that Congress would like to repeal.

- For Congress to pass a new law repealing a regulation outright, under current rules, it cannot bypass the filibuster and would require 60 votes in the Senate.

- However, either zeroing out penalties or creating a tax credit as described here could be done through reconciliation, bypassing the filibuster and allowing Congress to effectively remove certain regulatory burdens by removing the monetary penalty enforcement.

- Zeroing out penalties would be ideal but would require much more expansive reconciliation instructions and more complicated coordination amongst congressional committees to draft the legislation. It would be far simpler, faster, and easier to create a catch-all tax credit.

- Additionally, if penalties are lowered to close to zero or if the tax credit is almost equal to the size of the penalties, then businesses would be able to engage in covered activities while paying a modest and manageable amount of net penalties – included with the offsetting tax credit. As a result, this provision could act as a pay-for since the increase in penalties collected would be slightly in excess of tax credits paid out while also achieving the desired deregulatory goals.

Improve Multiemployer Pension Solvency

Background: Prior to a roughly $100 billion select taxpayer bailout in 2021, multiemployer, or private union, pensions had accumulated $823 billion in unfunded pension promises and were on track to pay workers only 41 cents of every dollar in promised pension benefits. While the bailout delayed some plans’ insolvency, multiemployer pensions still have $721 billion in unfunded liabilities that keep growing because plans continue to overpromise and underfund pension benefits.

Congress should:

- Increase the Pension Benefit Guaranty Corporation’s (PBGC) flat-rate multiemployer premium at least three-fold, from $40 to $120 per year.

- Add risk-based insurance premiums to PBGC’s multiemployer program.

- Impose an unfunded liabilities stakeholder fee of $8 per month per worker on each of the three multiemployer stakeholders: employers, unions, and pension participants.

WHY THE BUDGET RESOLUTION MATTERS

BACKGROUND

Before Congress can consider and pass a reconciliation bill, it must adopt a budget resolution that unlocks the process through what are known as reconciliation instructions. It is similar to getting approved for a car loan before picking out the exact car you want – in the same way that it is important that the loan be affordable and able to cover the car you want, the reconciliation instructions limit what can be done and define what must be done within a reconciliation bill. Getting the right instructions in a budget resolution is just as important as the subsequent debate over the reconciliation bill itself.

Budget Resolution Trade Offs

For a reconciliation bill to include many policies items, the budget resolution must include instructions to several committees – which can make the process more complicated and take longer to get through Congress.

A draft budget resolution has been introduced that would provide narrow reconciliation instructions only to the homeland security and Judiciary committees in the House and Senate. This draft would allow only for up to $70 billion in DHS funding to be included in the bill. Narrowing the scope of reconciliation could help expedite its passage through Congress and maximize the chance of getting the DHS funding signed into law in time to fully continue vital DHS operations before current funding is exhausted. However, if left unamended, this narrow set of instructions would miss the opportunity to enact a multitude of beneficial reforms.

Budget Resolution Options

Even still, it may be possible for Congress to:

- Subsequently amend this budget resolution – after passing a first reconciliation bill – to generate a new set of instructions for a new bill later this year; or to

- Pass and adopt the budget for the next fiscal year early enough to pass a second, more expansive, reconciliation bill later in this calendar year.

Nevertheless, these options would require Congress to vote on and adopt a second budget resolution in order to unlock the ability to pass a second reconciliation bill, which complicates the situation and reduces the chances of it happening.

Ideally, Congress should provide a single set of expansive budget instructions and pass a single sweeping bill. However, if the congressional majority insists on a fast-tracked and narrow DHS bill upfront, there is another option for the budget instructions.

- Pass a budget resolution that includes instructions for two different reconciliation bills. In particular, the current draft resolution could be amended to maintain its present Homeland and Judiciary instructions expressly for a first bill and then provide instructions specifically for a second bill to alter revenue levels with instructions to other committees, in particular the Senate Finance Committee and House Ways and Means Committee. This would allow for just one budget vote to be used to generate a fast-tracked DHS funding bill and then a subsequent bill with revenue-only provisions.

Budget Resolution Options

Something similar was done in a budget resolution in 1997 that was then used to create instructions for two reconciliation bills, one focused on altering spending levels and another focused on altering revenue levels.

Returning to the earlier analogy, this would be like getting approved for a loan that could finance two cars – a small quick vehicle to get funding to DHS and another larger one that can carry the whole family of pro-growth and anti-fraud reforms.

However, it should be noted that in 1997, both bills included changes to both spending and revenue levels. The federal statute governing the reconciliation process would still allow such a set of bills and, at the time, the parliamentary precedent allowed for multiple reconciliation bills – generated from the same budget reconciliation instructions – to each address both spending and revenue levels. Subsequently, parliamentary precedent has come to view this as opening the door to gaming against the intent of the reconciliation process and now would still allow two bills but would require that one address spending and the other only revenues – cleanly separating the two.

This potentially leaves open the door for Congress to try to return to an originalist approach, that upholds the statutory law governing the process, and satisfy the issue that later parliamentarians retroactively developed with the 1997 approach.

Additional Potential Option

The 1997 budget resolution was unclear as to which spending and revenue targets, and which committees, would be included in which of the two bills it envisioned. This murkiness is what parliamentarians thought opened the process to gaming through potentially allowing unlimited reconciliation bills.

Instead, Congress could now attempt to write clean budget instructions to just the homeland security and Judiciary committees for a spending-only first bill and then could provide instructions for other committees for both spending and revenue provisions in a second bill. This would comply with the federal statute governing the reconciliation process and may satisfy the parliamentarian’s issue. However, it would, at present, require a ruling from the parliamentarian.

It should also be noted that the Constitution ensures that a simple majority of each chamber of Congress can set its own rules and the majority of the Senate can overturn a ruling of the parliamentarian that they believe is incorrect or doesn’t properly uphold the actual federal statutes governing the reconciliation process.

Conclusion

While it would be ideal to do everything together in one reconciliation bill, if Congress wants to focus first on purely providing DHS funding, it should at the very least set up the budget reconciliation instructions to allow for the creation of two bills – one for DHS spending and one for revenue provisions, and perhaps more. This could still allow Congress to fast-track DHS funding while preserving the ability to do a broader second bill without requiring another complicated budget resolution debate and series of votes.