Policy Memo

Topline

The One Big Beautiful Bill (OBBB) permanently extended the expiring pass-through deduction for mostly small business owners, avoiding a looming tax hike of up to 20% on business income.

The One Big Beautiful Bill (OBBB) permanently extended the expiring pass-through deduction for mostly small business owners, avoiding a looming tax hike of up to 20% on business income.

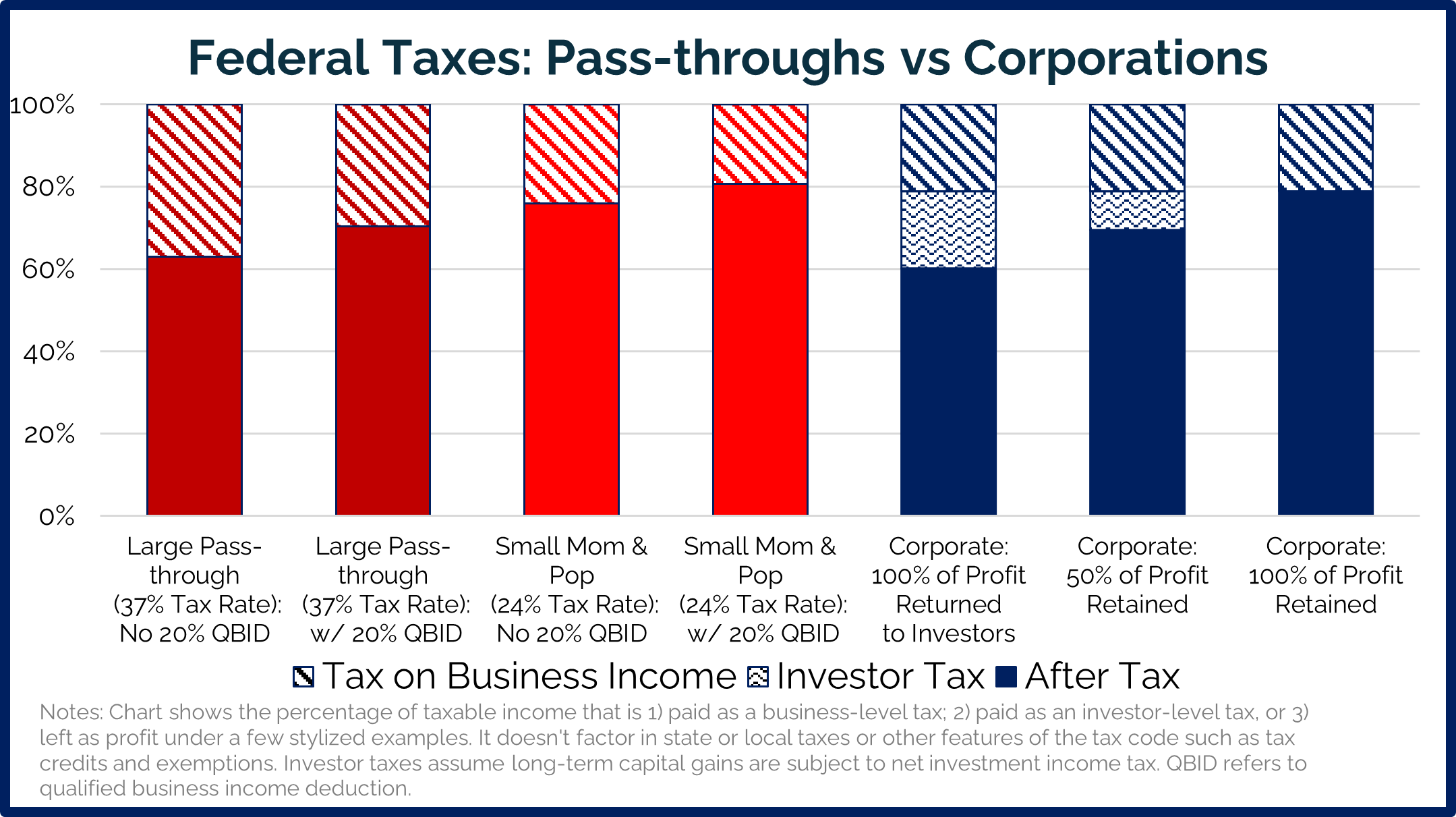

For tax purposes, there are two main types of businesses. Publicly traded companies with more than 100 shareholders are typically organized as corporations, while most smaller companies (e.g., sole proprietors, partnerships, and “S-corporations) are “pass-through” businesses. The tax code offers different tax treatments for each. Corporations pay corporate profits, and then when the after-tax returns are ultimately transferred to shareholders, they are taxed again at the investor level as capital gains or dividends. On the other hand, pass-through profits “pass through” to the shareholders as the profits are earned and are immediately taxed as business income on their individual returns—there is no extra investor-level tax.

The 2017 Tax Cuts and Jobs Act (TCJA) reduced the corporate tax rate from 35% (near the highest in the developed world) to 21%, but left in place the top tax rate on long-term investor gains of 23.8%. TCJA reduced taxes for individuals with pass-through business income in two ways: (1) It reduced individual tax rates, including the top tax rate from 39.6% to 37%; and (2) it added a 20% qualified business income deduction (QBID). TCJA’s changes reduced the top effective tax rate on qualified pass-through income from 39.6% to 29.6%. Individuals with business income from certain service industries where the main asset is the talent and reputation of employees faced special limitations, where QBID started phasing out for those with (inflation-adjusted) incomes of more than $157,500/$315,000 (single/married joint filers) of such service income and fully phased out over a range $50,000/$100,000 above that threshold.

The effective tax rate of pass-through business owners depends on their taxable income and whether they qualify for the pass-through deduction. Corporations face a flat federal corporate tax rate, but investor-level tax rates depend on income and whether gains are short or long-term. When corporations retain earnings or reinvest into the company, it allows shareholders to defer investment taxes (temporarily).

Pass-through tax treatment is more favorable than corporate tax treatment in many—but not all—situations. The chart below illustrates a few cases.

OBBB Sec. 70105; 26 U.S.C. § 199A.

The pass-through deduction is complicated and not ideal policy. It’s a workaround that allowed Congress to cut taxes in 2017 to a comparable degree for pass-throughs as they did for corporations. But whatever the deduction’s shortcomings, allowing a major tax increase on businesses wasn’t the answer. Many small business owners are breathing a major sigh of relief that Congress extended the deduction. Going forward, Congress should strive for corporate integration—alignment of the tax treatment of pass-through businesses and corporations.

This memo is part of the One Big Beautiful Booklet, a collection of more than 60 memos that examine and summarize the major aspects of the One Big Beautiful Bill – the signature legislative achievement of President Trump and the 119th Congress.

more ob3-60 memos