Policy Memo

Topline

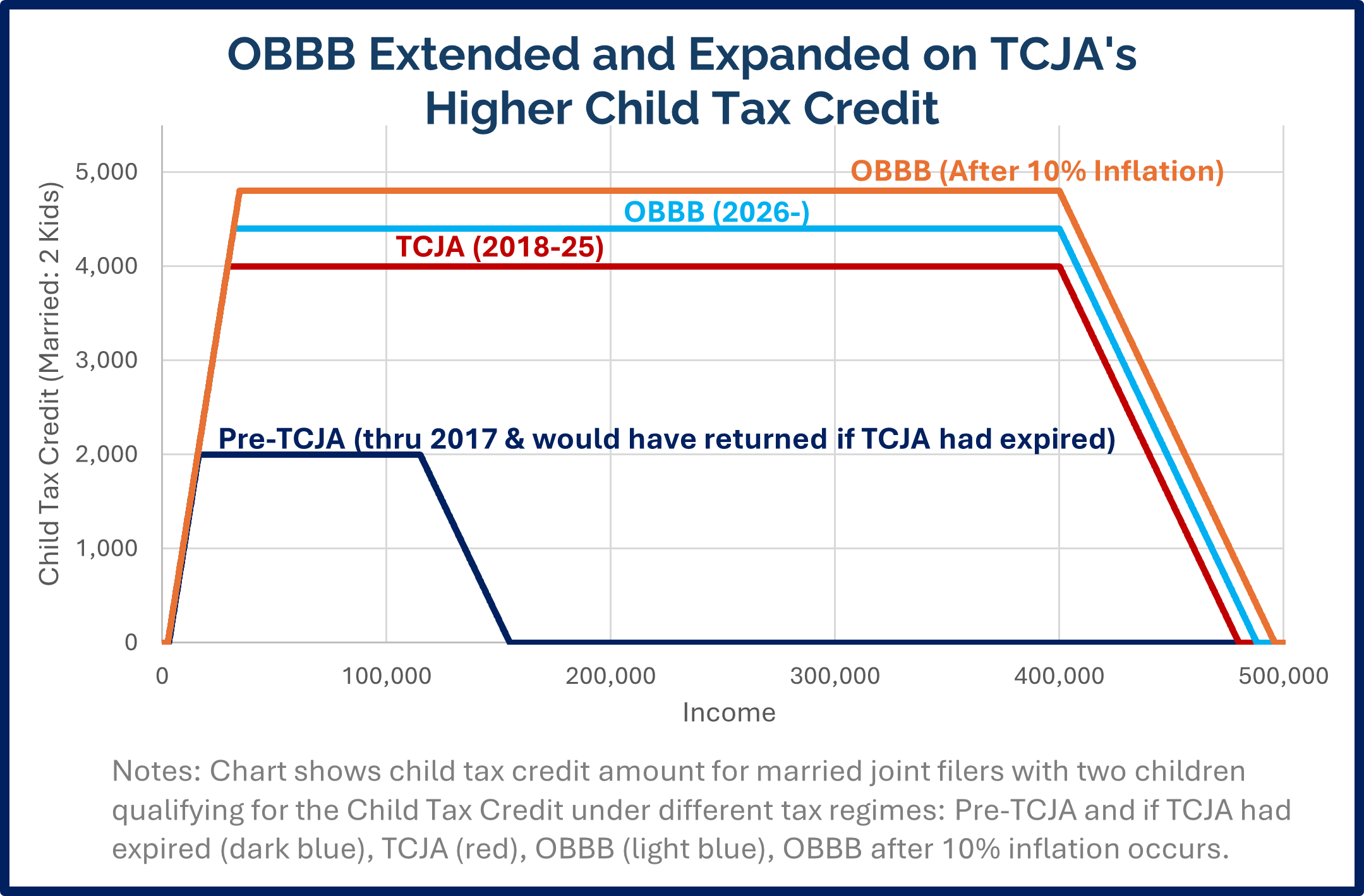

The OBBB expanded and made permanent the Child Tax Credit, providing meaningful tax relief to American families.

The One Big Beautiful Bill (OBBB) permanently extended the 2017 Tax Cuts and Jobs Act’s (TCJA’s) Child Tax Credit changes, including its doubling of the credit amount and less restrictive phase-in and phase-out. OBBB also added $200 more to the credit and added an automatic inflation adjustment to the credit amount.

Prior to the 2017 tax bill, the tax code allowed individuals to claim a $1,000 tax credit per qualifying child ages 16 and under. The credit was partially refundable, meaning that some taxpayers with no net income tax liability could claim part (or in some cases all) of the credit amount, getting a tax “refund” that was greater than the income taxes they paid during the year. The Child Tax Credit effectively began phasing in for taxpayers with at least $3,000 of earned income and phased in at a rate of 15% for earned income above that amount until maxing out at $1,000 per child. The Child Tax Credit then began phasing out at a 5% rate for income beyond a threshold of $75,000/$110,000 (single/married joint filers).

For the tax years 2018 through 2025, TCJA:

OBBB Section 70104; 26 U.S.C. § 24(h)-(i).

It makes sense for the tax code to have a Child Tax Credit or some other mechanism to reduce taxes for larger families, given the level of progressivity in the U.S. tax brackets. The strain on families’ financial resources increases as the number of mouths to feed increases. However, the Child Tax Credit is now large enough that the tax code is more favorable to taxpayers with children than to those without, all else being equal. Adding to the Child Tax Credit beyond OBBB’s changes would go too far. Many childless young couples want to have children one day—the tax code shouldn’t be biased against them in the meantime.

In theory, the Internal Revenue Service exists to collect tax revenue, not to administer benefits. Refundable tax credits like the Earned Income Tax Credit, the refundable portion of the Child Tax Credit, and various recent stimulus payments administered by the IRS have blurred that distinction as some taxpayers’ tax “refund” checks dwarf the taxes they pay.

This memo is part of the One Big Beautiful Booklet, a collection of more than 60 memos that examine and summarize the major aspects of the One Big Beautiful Bill – the signature legislative achievement of President Trump and the 119th Congress.

more ob3-60 memos